Welsh government plans to tweak relief for buyers

Welsh government plans to tweak relief for buyers The draft Welsh Budget 2026/27 confirmed there would be no changes in the rates of land transaction tax. However, it did reveal some related changes are being planned. What’s the full story? Land transaction tax (LTT) is the devolved equivalent of stamp duty land tax in Wales. It operates in a broadly similar way, but the Welsh Government has the power to set the rates and bands. The draft Budget document confirms that there is no intention to change the rates and bands for residential and non-residential property. However, there will be changes to other parts of LTT. Get the extra help you Need Firstly, a new “equalisation” rule will be introduced to the multiple dwellings relief rules. It appears this will provide for an adjustment where properties subject to a claim are chargeable at both the main and higher rates. More detail is expected next month. There will also be an increase in the minimum tax rule rate from 1% to 3%. This rule sets a floor so that the amount of tax collected cannot be less than the specified percentage. Finally, an additional refund rule will apply to higher rate transactions where a landlord leases the property to a local authority in Wales via the Leasing Scheme Wales. This will allow the buyer to obtain a refund of the additional charge in a similar way to someone replacing their main residence. It is expected that, if approved, the changes will apply from April 2026. back to the menu top If you would like any assistance with any of these points. Please Call Us on 0161 872 8671 Get in Touch Want a financial consultation with no obligation? Call Dunhams Chartered Accountants now on 0161 872 8671 Or email paul.o’brien@dunhams.co.uk or andrew.edwards@dunhams.co.uk

MONTHLY FOCUS: PENSIONS AND INHERITANCE TAX

MONTHLY FOCUS: PENSIONS AND INHERITANCE TAX Starting in April 2027, all unused pension funds will be pulled into the inheritance tax (IHT) net. In this Monthly Focus, we look at the proposed changes and how they might affect your estate’s IHT liability. Page Content:- Current Position Pensions and IHT from April 2027 TAX PLANNING CURRENT POSITION What’s the IHT position on pension savings before April 2027? IHT doesn’t usually apply when you pass on your pension rights, which can be a pot of cash and investments or the right to a pension, including any associated lump sum. This applies whether you die before you start taking your pension savings or after. In fact, unlike other types of investment, your pension fund(s) aren’t normally part of your estate, they are held in trust. Most pension savings, whether or not they are held in a registered scheme (one approved by HMRC), are held in discretionary trusts. The trustees decide who is entitled to a share of the money and other assets held by the trust. In practice, they earmark the funds for the person who pays into the pension and, on their death, their nominated beneficiaries. Further, the IHT legislation (Inheritance Tax Act 1984) says that transfer of pension savings you may have been entitled to and which are paid to your beneficiaries on your death don’t count as a transfer for IHT purposes. In plain English, this means they are exempt from IHT. What types of pension scheme currently escape IHT? The current IHT exemption applies to all registered pension schemes subject to the exceptions mentioned below This includes: personal pension schemes (including self-invested personal pensions) workplace pensions required under the auto-enrolment rules – these might be group personal pensions or hybrid final salary type schemes stakeholder pension plans additional voluntary contribution (AVC) plans and freestanding AVCs final salary schemes. These days they are mostly for civil servants, and those working for the NHS and government bodies. The exemption also apples to qualifying recognised overseas pension scheme. These are typically paid into by individuals who have lived or worked abroad. You’ll know if you have one. Also exempt are pension savings in non-registered schemes such as funded unapproved retirement benefit schemes and funded employer-financed retirement benefit schemes where the pension savings and rights to benefits are held in discretionary trust. Get more Help and Assistance from our Accounting Services Get in Touch Want a financial consultation with no obligation? Call Dunhams Chartered Accountants now on 0161 872 8671 Or email paul.o’brien@dunhams.co.uk or andrew.edwards@dunhams.co.uk Are there circumstances where IHT might be payable on pension savings? Yes, there are a number of situations where IHT can apply. Non-discretionary pension rights If the pension scheme is obliged to pay you or your beneficiaries a pension or lump sum, i.e. the payment is not at the discretion of the scheme administrators or trustees, the value of the pension rights will be part of your estate for IHT purposes. The types of pension scheme to which these apply are: so-called buy-out plans, also known as Section 32 plans. These are a type of personal pension plan where a pension company accepts a transfer of your pension benefits under a scheme linked to your employment (an occupational scheme) particularly if the scheme being bought out is being wound up or you leave the employment to which the pension relates. You’ll probably know if you have a Section 32 plan but if you’re unsure check with the pension company or financial advisor retirement annuity contracts (Section 226 contracts). These were the predecessor to personal pension plans. They ceased to be available in July 1986. However, the benefits from these could and often were placed into an individual discretionary trust and so like personal pensions they could escape the IHT net certain types of occupational scheme, typically those set up for company owner managers or directors and senior employees, and some statutory schemes. Again, you’ll probably know if you have one of these. The two-year rule If you’re in poor health which you expect to shorten your life and you deliberately avoid accessing your pension savings or benefits so that more is left in your IHT-exempt pension fund, e.g. you defer taking an occupational pension (that’s a pension linked to your employment), IHT may be payable on the amount of pension income you could have taken. The sort of action that might cause deferral of pension benefits that HMRC might be looking out for are, where in the two years before death you: transfer your pension benefits to another scheme pay in significant extra pension contributions; or transfer benefits in a Section 32 or Section 226 contract to a discretionary trust. Whoever is administering your estate, e.g. the executors, must report this type of transaction to HMRC on Form IHT409. What about income tax on inherited pension savings? After you die the pension company will pay your pension savings or regular pension to the persons you nominated as beneficiaries. Whether or not the payment is taxable depends on how old you were: if you die aged 74 or younger the whole pension savings are tax free for your beneficiaries if you die aged 75 or older, the pension savings are taxable as income. Where the pension payments are taxable they count as additional income for your beneficiaries whether taken as a lump sum, spread over several or more years or paid out as a lifetime pension. Note that your beneficiaries don’t get the 25% tax-free amount that you’re entitled to when you receive a pension during your lifetime. Pensions and IHT from April 2027 What’s changing and when? From 6 April 2027 an individual’s savings held in a pension fund will in nearly all circumstances be included in the value of their estate when they die. There are exceptions, e.g. a death in service pension and benefits. The draft legislation refers to “discretionary” pension savings, as it’s these that currently escape the IHT net. Discretionary means

Recovering salary overpayments due to payroll errors

Recovering salary overpayments due to payroll errors Five employees at Glasgow City Council have together been ordered to pay back £40,000 in overpaid wages caused by a payroll error relating to the calculation of their contractual overtime. If you overpay wages to an existing employee due to a payroll error, can you recover them? Where the purpose of a deduction from an employee’s wages is to reimburse you in respect of a previous mistaken overpayment of wages, the unlawful deductions from wages regime in the Employment Rights Act 1996 doesn’t apply. This means you can lawfully recover the overpayment by making deductions from the employee’s future wage payments, even if there’s no contractual clause allowing it, and you don’t need their consent. Get the Payroll Assistance with Dunhams In this situation, you should notify the employee as soon as possible of the overpayment. Explain the error in writing, give details of the overpayment and how it has been calculated and then set out how you propose to recover it, i.e. by deducting sums from their wages. If the amount of the overpayment is large, it’s advisable to propose a reasonable repayment plan under which wage deductions are phased over several pay periods, rather than just deducting it all at once, to avoid causing financial hardship for the employee. Aim to agree this repayment plan with the employee. When you then make the relevant wage deductions, itemise these clearly on payslips – include the amounts of, and reasons for, the deductions. back to the menu top If you would like any assistance with any of these points. Please Call Us on 0161 872 8671 Get in Touch Want a financial consultation with no obligation? Call Dunhams Chartered Accountants now on 0161 872 8671 Or email paul.o’brien@dunhams.co.uk or andrew.edwards@dunhams.co.uk

Salary transparency on recruitment

Salary transparency on recruitment A pay transparency survey has revealed that 70% of employers intend to share salary ranges with external candidates during recruitment ahead of the EU Pay Transparency Directive coming into force. Will this become a legal requirement? There is currently no legal requirement in the UK to include salary details, or salary bands, in job adverts. However, the following developments are of relevance: Get the Accountancy Services You Need here. Even if UK law on pay transparency during recruitment doesn’t change, if publishing salary ranges in job adverts starts to become the expected “norm” as a result of a cultural shift, then you may have to follow suit to ensure you continue to receive sufficient job applications from high-quality candidates. If you do include a salary range, also consider setting out information about your benefits package. Alternatively, you could state that salary information will be provided before interview to those candidates who are selected to progress to that stage. back to the menu top If you would like any assistance with any of these points. Please Call Us on 0161 872 8671 Get in Touch Want a financial consultation with no obligation? Call Dunhams Chartered Accountants now on 0161 872 8671 Or email paul.o’brien@dunhams.co.uk or andrew.edwards@dunhams.co.uk

HMRC scrutinising directors’ loans

HMRC scrutinising directors’ loans HMRC has begun a new compliance campaign targeting company directors who owed their companies money. What’s the full story, and how should you respond? Warning letter HMRC says that it will shortly write to all directors that it has identified as having had one or more loans from their companies which were written off or released (waived) between April 2019 and April 2023. You’ll receive a letter if you didn’t report the details on your self-assessment tax return or notify HMRC by other means. The likelihood is that you’ll have further income tax to pay. For more Help see our Accounting Services Taxable income When a company writes off or waives a debt owed to it by an employee, director or shareholder it counts as taxable income. The write-off or release of a debt might be taxable as earnings or, in the case of a director who’s also a shareholder, as a distribution which is taxed in the same way and at the same tax rates as a dividend. The tax payable is lower for a written off or waived debt taxed as a distribution compared to the tax as earnings. Which of these applies depends on whether the debt arose by reason of your employment or because you’re a shareholder. If the debt arose by reason of employment, the company should have reported it and accounted for Class 1 NI. If it hasn’t your company might also be in hot water with HMRC. Action required If you’re already aware that you have overlooked reporting a written off or waived debt to HMRC, or become aware because you receive a letter from HMRC, you should report it in one of two ways. If the write-off/waiver occurred after 5 April 2023, amend your 2023/24 self-assessment tax return or, if it occurred earlier (or if it relates to 2023/24 but you didn’t complete a tax return for that year), use HMRC’s online disclosure service. Volunteering the information rather than waiting for HMRC to pressure you can reduce any financial penalty it might charge. Get in Touch Want a financial consultation with no obligation? Call Dunhams Chartered Accountants now on 0161 872 8671 Or email paul.o’brien@dunhams.co.uk or andrew.edwards@dunhams.co.uk If you would like any assistance with any of these points. Please Call Us on 0161 872 8671

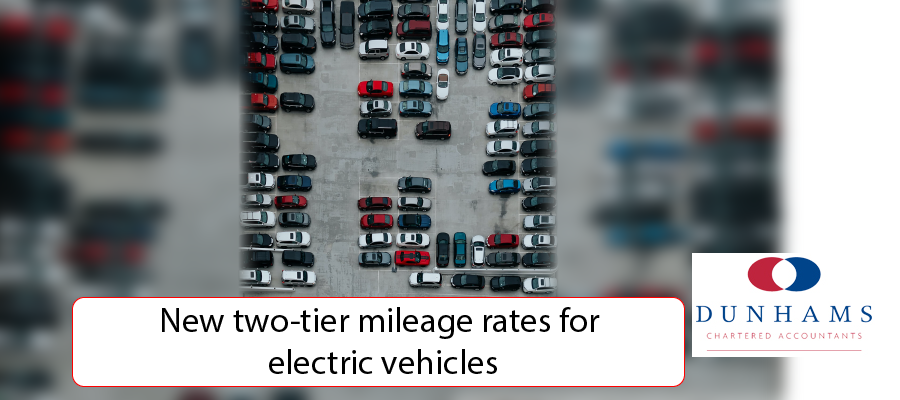

New two-tier mileage rates for electric vehicles

New two-tier mileage rates for electric vehicles The amount that employers can reimburse staff for business travel in company cars changes from 1 September 2025. What are the new rates, and why is this update different to previous ones? Advisory fuel rates for company cars are updated by HMRC on a quarterly basis due to fluctuations in fuel prices. The rates determine the amount that can be paid to an employee using a company car for business mileage, or where an employee has to reimburse their employer for private journeys. Where HMRC’s rates are used, there are no income tax consequences for the employee. HMRC has now published the advisory rates applicable from 1 September 2025. The rate per mile will be: Get the Accounting Services you need here Engine size Petrol LPG 1,400cc or less 12p 11p 1,401cc to 2,000cc 14p 13p Over 2,000cc 22p 21p Engine size Diesel 1,600cc or less 12p 1,601cc to 2,000cc 13p Over 2,000cc 18p The big difference this time is the introduction of a second electricity rate for fully electric cars. For 1 September, the two rates will be: 8 pence per mile for home charging 12 pence per mile for public charging back to the menu top If you would like any assistance with any of these points. Please Call Us on 0161 872 8671 Get in Touch Want a financial consultation with no obligation? Call Dunhams Chartered Accountants now on 0161 872 8671 Or email paul.o’brien@dunhams.co.uk or andrew.edwards@dunhams.co.uk

Temporary workers – your pension obligations

Temporary workers – your pension obligations If you’re employing temporary workers for the summer season don’t forget that they have the same rights to join your workplace pension as permanent employees. What do you need to do? Pension auto-enrolment Workplace pensions have been around for over a decade. Despite this, every year some employers forget that temporary employees they take on, say during the summer period, have the same rights to workplace pensions as their full-time workers. Because of this HMRC is currently running a campaign to remind employers. Get more information on our Accounting Services Pages. Assess and advise If you’re an employer you must assess temporary staff for their right to be enrolled in your workplace pension scheme each time you pay them, even if they only work for you for a few days. If you don’t assess your employees for entitlement to join your workplace pension it can result in a warning from HMRC or The Pensions Regulator. This can escalate to a fine of £400 initially and then daily penalties of between £50 and £10,000. You can avoid having to assess your employees if they will work for you for no more than three months. Do this by using the auto-enrolment postponement procedure. back to the menu top If you would like any assistance with any of these points. Please Call Us on 0161 872 8671 Get in Touch Want a financial consultation with no obligation? Call Dunhams Chartered Accountants now on 0161 872 8671 Or email paul.o’brien@dunhams.co.uk or andrew.edwards@dunhams.co.uk

Opt out of winter fuel payments by 15 September

Opt out of winter fuel payments by 15 September HMRC has issued new guidance on the winter fuel payments. What do you need to know? The winter fuel payment will be paid to state pension recipients this winter and is worth £200 per household, or £300 if you’re over 80. Find the Help you Need on our Accounting Services Pages Eligible pensioners will receive a letter in October or November, with the payment being made automatically in November or December. New details have been released on the eligibility criteria, including a useful tool to check whether your income is over the threshold of £35,000. If it is, you’ll still receive the payment, but it will be clawed back using the tax system. The tool will confirm how the payment will be recovered if applicable. If you’d prefer to opt out you can do so using this form, but it must be done before 15 September 2025. back to the menu top If you would like any assistance with any of these points. Please Call Us on 0161 872 8671 Get in Touch Want a financial consultation with no obligation? Call Dunhams Chartered Accountants now on 0161 872 8671 Or email paul.o’brien@dunhams.co.uk or andrew.edwards@dunhams.co.uk

MONTHLY FOCUS: THE KEY TAX CONSIDERATIONS FOR A NEW BUSINESS

MONTHLY FOCUS: THE KEY TAX CONSIDERATIONS FOR A NEW BUSINESS In this monthly focus, we take a look at the tax matters that affect new unincorporated businesses in the first year, including dealing with HMRC, the choice of accounting basis, deductible expenses, and dealing with losses. Page Content:- BEFORE BUSINESS BEGINS WHEN TRADE COMMENCES THE FIRST TAXABLE PERIOD LOSSES BEFORE BUSINESS BEGINS Starting up The first key tax date for any business is that on which it opens its doors to customers. HMRC refers to this as the date on which trade commences. It’s important because it’s the point from which HMRC starts to measure the profits and losses on which you’ll pay income tax and National Insurance (NI). However, no business starts overnight. At the very least you must decide what to call your business, make agreements with business partners as well as taking practical steps, such as setting up a bank account and a means of getting paid by your customers. The lead-in time for getting a business ready to trade can vary significantly; it might be just a few days if you’re setting yourself up as a consultant and working for just a few clients you already know, or it can last months if you’re starting a manufacturing business requiring premises and the installation of heavy machinery. It’s likely that every business will incur expenses before its trade commences. Without special rules some of these might not qualify for a tax deduction. More help for you Business – see Our Accounting Services What are the tax rules for pre-trading expenses? In a nutshell, the rule for pre-trading expenses allows you to claim a tax deduction for costs relating to your business if they would have qualified for a deduction had you incurred the expense after trading commenced. The rule says that pre-trading expenses are treated as if they were incurred on the first day business commences. You can claim a tax deduction for costs incurred up to seven years before your trade commences. For example, if your trade commenced on 1 May 2025 expenses back to 1 May 2018 can qualify. Get in Touch Want a financial consultation with no obligation? Call Dunhams Chartered Accountants now on 0161 872 8671 Or email paul.o’brien@dunhams.co.uk or andrew.edwards@dunhams.co.uk Can a deduction be claimed for personal expenses? The general rule is that no tax deduction is allowed for expenses if they aren’t incurred “wholly and exclusively for the purpose of a trade”. That’s a reasonable and understandable restriction. However, there’s a unique angle to pre-trading expenses which can allow a deduction for costs that might originally not have been incurred with your business in mind. You might have spent money on an item long before you thought about starting a business, but if it was later used for your business and the expense was incurred within the seven-year time limit, the pre-trading rule allows you to claim a tax deduction for it. Pre-trading expenditure will mostly relate to equipment, for example a car, but the same rules apply to smaller and less obvious items. Example John was employed as a designer with a kitchen company. In early 2025 he decides to start his own furniture design firm which he’ll run from an office in his home. In late 2020 he bought new IT equipment and furniture for his home office, which he used almost entirely for private purposes. In mid-2022 he bought a stock of paper, ink cartridges and stationery for his private use. John can claim a tax deduction under the pre-trading expenses rule for the IT equipment and the paper, ink, etc. How much tax deduction can I claim? Naturally, the amount of tax deduction depends on the cost of an item. Consumables bought pre-trading specifically for your business will be unused when trading starts and so the tax deduction is equal to the cost. However, if the item is durable (for tax purposes this means something that can be used multiple times for a period of two years or more, this is referred to as capital expenditure), e.g. equipment, it might be used or unused or have been bought for the business or for another purpose. The tax relief is allowed for: the cost where the item was bought for the business and unused; or the “market value”, i.e. the amount you could expect to receive if you sold it to someone unconnected to you, of the item if it was previously used for a purpose other than for your business. Tax relief can be claimed for the market value of equipment etc. bought by someone else, for a private purpose, but which you start using for your business. For example, a computer bought for you as a gift which you later start using for your business. Does the pre-trade rule apply to all expenses? No. You don’t need to rely on the pre-trading rule to obtain a tax deduction for stock and materials bought before trade commences if they were purchased specifically for the business. Normally, general accounting rules mean that these types of cost are included as an expense in your first accounts anyway and the tax rules follow the accounting rules in this instance. What about services I pay for before trading? The same pre-trading rule applies to services as it does to goods. However, in practice it will only be relevant to purchases made specifically for your business. For example, if you take a lease on a retail unit with the intention of running your business from it, you’re unlikely to start trading there on the day you receive the keys; it might need fitting out or other work before you can use it. While your accountant might include the rent for this period, along with the fitting out costs, in your business’s first accounts, for tax purposes they are pre-trade expenses. Are there any NI issues to consider for pre-trading expenses? You don’t need to register to pay self-employed NI, Class 2 and Class 4, until after you have started trading. Class 4 NI is

Change to IHT on pensions proposals

Change to IHT on pensions proposals HMRC has published a policy statement announcing an important change to its plans to include pension savings in an individual’s estate for inheritance tax (IHT) purposes. What’s the full story? In her first budget last Autumn Rachael Reeves dropped a number of bombshells. Find the Help You Need with Our Accounting Services. One of the biggest was her proposal to bring pension savings and death benefits within the scope of IHT from 6 April 2027. Currently, IHT only applies in very few circumstances. Where it does the pension companies may be responsible for calculating and deducting any IHT payable before passing the pension savings to the deceased’s beneficiaries. The Chancellor wanted to emulate this process when the new IHT rules were rolled out in 2027. In a policy paper published on 21 July the government announced that the responsibility for calculating and paying IHT on pension saving will rest with the personal representatives of an estate, e.g. executors, and not pension companies. Although the consultation on the proposed new rules, which is open to everyone, doesn’t close until 15 September it had already become clear that the Chancellor’s original proposal was unrealistic. back to the menu top If you would like any assistance with any of these points. Please Call Us on 0161 872 8671 Get in Touch Want a financial consultation with no obligation? Call Dunhams Chartered Accountants now on 0161 872 8671 Or email paul.o’brien@dunhams.co.uk or andrew.edwards@dunhams.co.uk